PhonePe Business — product design across four sub-projects

End-to-end design ownership on India's largest merchant payment platform. This case study covers four sub-projects shipped under the PhonePe Business umbrella — each solving a distinct merchant problem, together forming a coherent product experience.

Merchants

Users

Post-Redesign

Monthly Revenue

FIG 0.0 — PhonePe Business · Merchant Home

FIG 0.0 — PhonePe Business · Merchant Home

The most visited screen was failing its users.

PhonePe for Business is where merchants onboard, collect UPI payments, access settlements, manage devices, and apply for loans. The home screen is the face of all of this — the most used, most interacted, and most sought-after page. Yet it was chaotic: no hierarchy, buried features, no revenue channel, and no reason for a merchant to feel the app was built for them.

No feature discoverability

Settle Now, loan eligibility, device management — all buried. Merchants couldn't find critical functions without multiple taps.

Settlement anxiety

Auto-settlements weren't initiated in edge cases but merchants received no notification — leading to rising support tickets and merchant distrust.

Revenue left on the table

SmartSpeakers, POS devices, loans, and shop insurance had no proper discovery surface. The home page wasn't functioning as a revenue channel.

Pure utility, zero ownership

Merchants used the app because they had to — not because they wanted to. No sense of the app being a companion to their business.

A companion to the merchant's business. Not a tool they're trapped in.

From the product brief: the app needed to help merchants conduct, manage, and grow their business — integrating different lines of business and generating revenue for both merchants and PhonePe. But critically, it had to do this without creating funnels that trap. Absolute clarity going in, and always a way out.

The merchant comes to the app because it's a NEED. Our job is to create the WANT. Good visuals, good experiences, good support — make them feel the app is for THEM, not US.

Critical functions upfront, always

Minimize clicks and rabbit holes. Every feature a merchant needs should be reachable from the home screen with the fewest possible taps.

Reimagine the entire IA

Don't patch the existing architecture. Rebuild it around the three things every merchant does: conduct their business, grow it, and manage it.

Make value-added services discoverable

Devices, loans, and insurance shown upfront with illustrations and clear benefit statements — informational, not pushy.

Powerful help, fast resolution

Merchants should be able to find solutions to all their problems in the shortest time — via a strong in-app support centre, not a call centre.

Merchants think in workflows, not features.

I ran heuristic audits on the existing home screen, analysed support ticket themes, reviewed analytics drop-off data, and conducted merchant interviews across business types and geographies. The clearest signal: merchants didn't think in terms of app features. They thought in terms of business activities — "did I get paid?", "is my money in my account?", "how do I get a loan?"

This insight became the structural foundation of the redesign: the framework of Conduct – Grow – Manage. Three verbs. Three zones. One clear mental model.

P2ML merchants visit at least once a month. P2P merchants get everything via notifications — they don't need to visit daily. The home screen had to earn engagement from users who didn't have a reason to open the app.

Any merchant who comes onto the app expects simplicity and ease of doing their business — timely validation of collections and payments made digitally.

Transactions

Validate payments and settlements seamlessly, with a detailed transaction and settlement history.

Settlements

Settle Now as a primary focus of the entire app — and auto-settlements shown in a clutter-free, easy-to-understand format.

Payment Analytics

Analyze sales performance and growth trends; generate reports for insights into expansion.

Once merchants have validation of what's happening, they want to grow. Value-added services shown upfront in an informational, clear manner.

Devices & Services

Explore, purchase, or lease devices; track orders and manage owned devices.

Loans

A clean, easy discovery point for business loans — the merchant's route to expansion.

Incentives

Promotions and discounts that nudge merchants toward services — visibility keeps them hooked.

Crucial for established merchants who have availed devices and services — their control panel.

Profile / Account

Business info, billing and payment settings, language and notification preferences.

Device Management

Manage owned devices, track orders, troubleshoot issues, pay device dues.

Loan Dashboard

Monitor loan status, outstanding balance, and upcoming payments.

Customer Support

In-app chat support for immediate help — with self-serve solutions first.

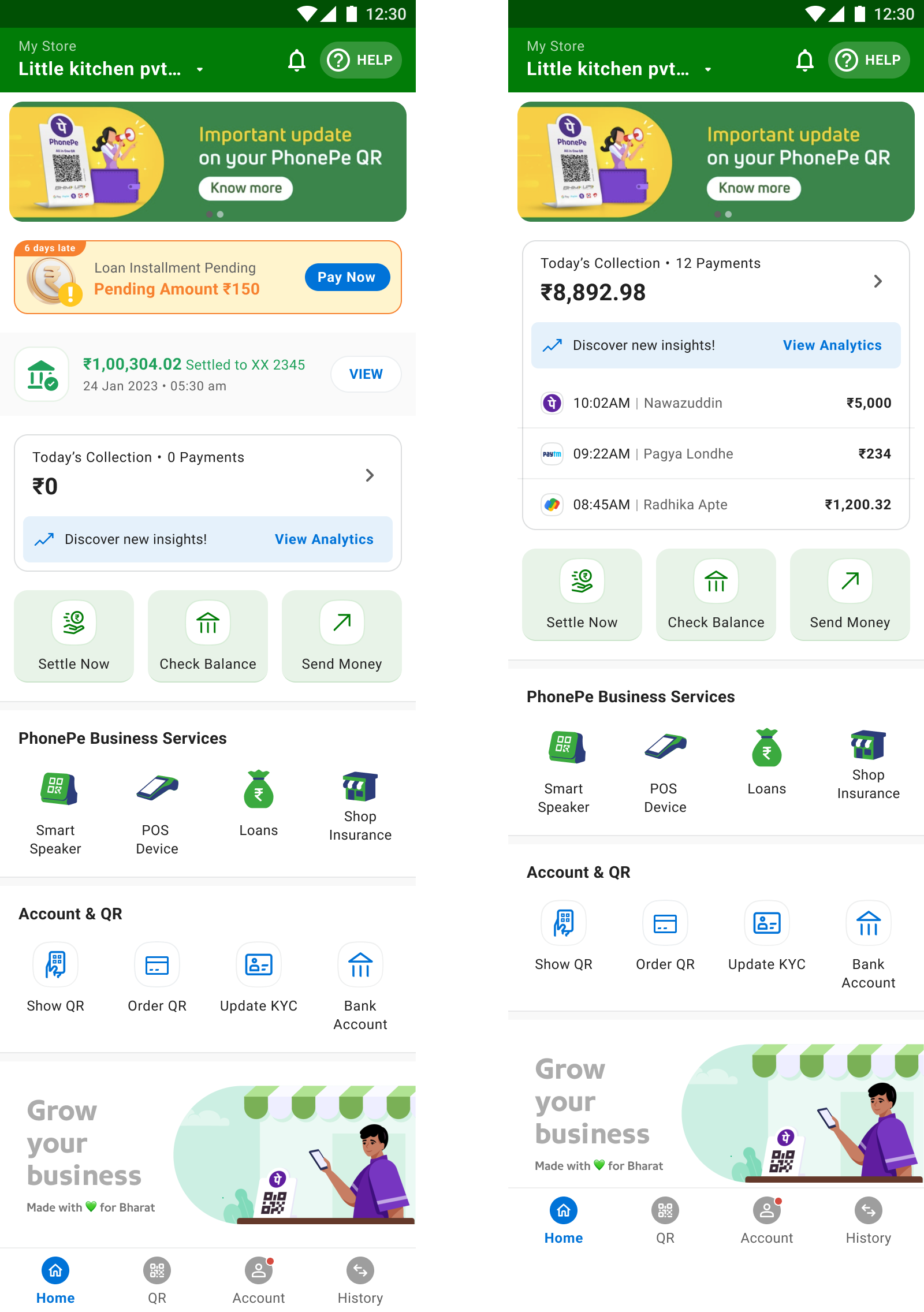

Conduct – Grow – Manage

FIG 4.0 — Before / After

FIG 4.0 — Before / After

Conduct

Any merchant who opens the app expects simplicity and ease. They need timely validation of payments, instant access to settlements, and a clear view of today's collections. Everything in this zone is about reducing friction for the core business activity.

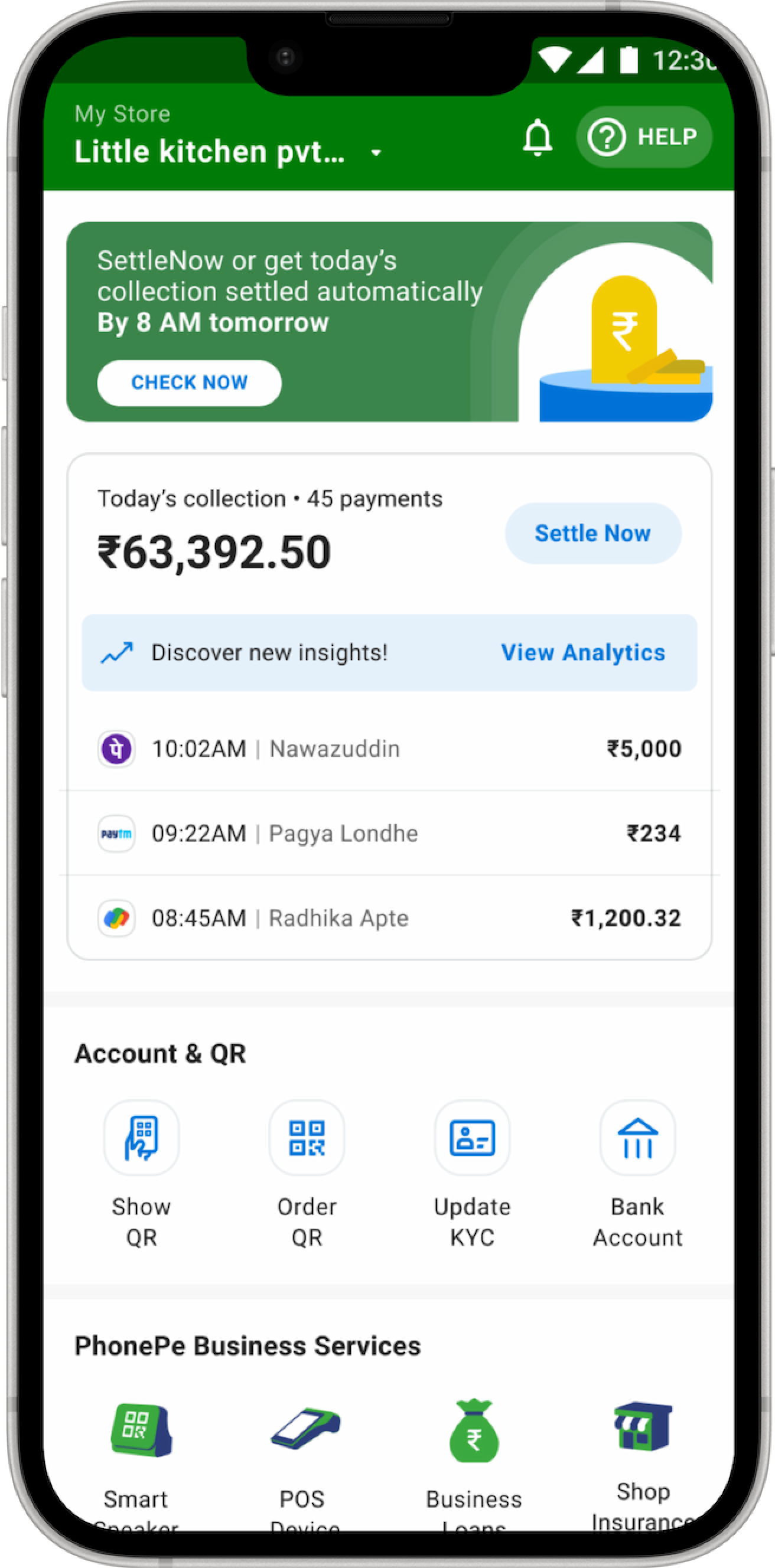

Today's Collection — hero metric

Total day's collection shown as the primary number on home, with recent transactions listed immediately below — no scrolling required to validate payments.

Settle Now — elevated

For the vast majority of merchants, getting money in their bank account is the best validation. Settle Now becomes a primary home-screen action, not buried in a flow.

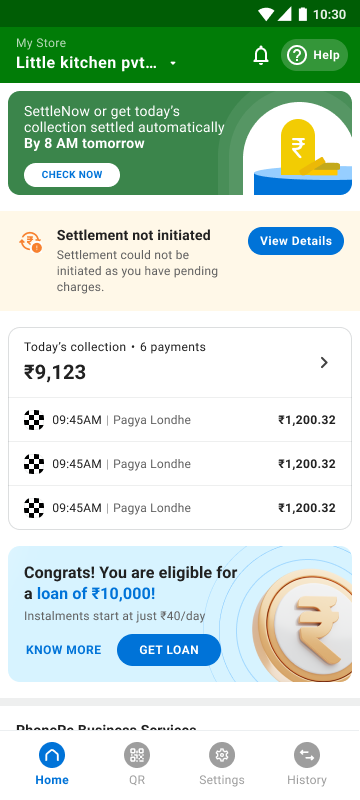

Settlement Not Initiated — transparent

Redesigned error messaging for settlement failures: clear ribbon on home, detailed breakdown on the settlement page, and deep-links to resolve pending charges.

Business analytics

Monthly collection with month-on-month comparison, 7-day chart, average daily collection, and transaction count.

Grow

Once merchants have validation of their daily business, they're open to growing it. Value-added services are surfaced in context — with illustrations that clarify what each product does.

PhonePe Business Services grid

SmartSpeaker, POS Device, Loans, Shop Insurance — shown with iconography and clear labels, accessible one tap from home.

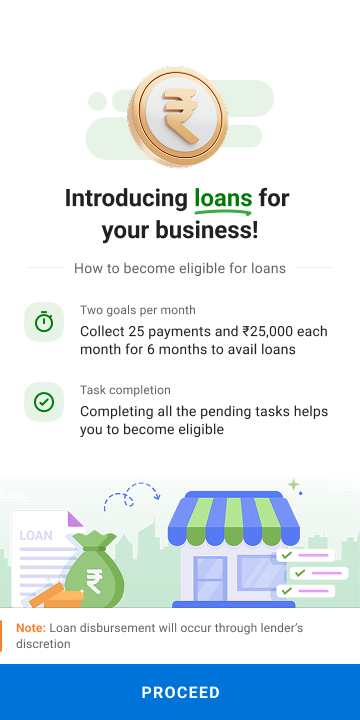

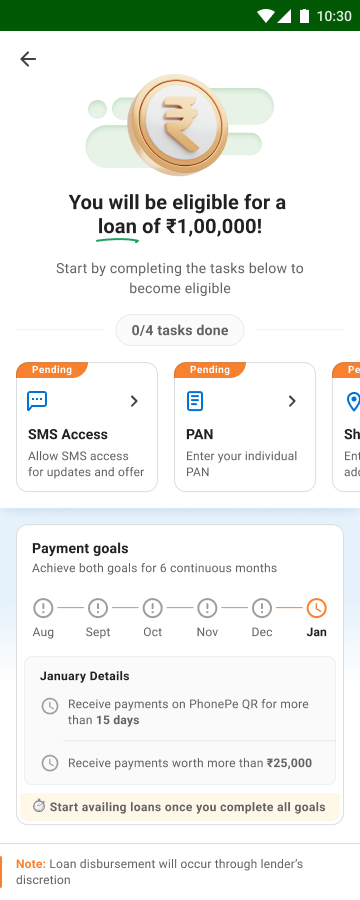

Business loans — eligibility flow

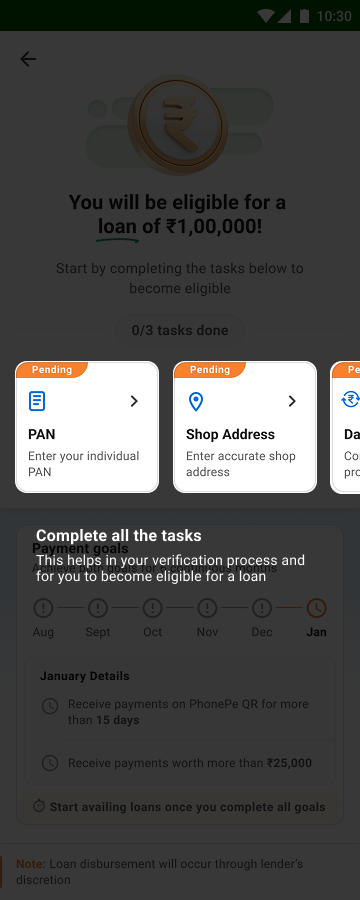

A dedicated eligibility journey with 3 sections: Tasks (one-time to-dos like PAN submission), Milestones (6-month payment targets), and Devices (maintain 0 dues). Gamified progress to drive return visits.

Hero nudge widget

Contextual banner slot for promoting the highest-priority offering at any given time — loans, new devices, or insurance — with illustration and a clear CTA.

Incentives & offers

Promotions surfaced with clear value statements — a nudge like "buy a speaker and save ₹500" goes a long way.

Discovery

Merchant notices a "Business Loan" widget on the home screen while checking transactions. High-intent entry point.

FTUE — first time use

Coachmarks explain the 3 sections of eligibility — Milestones, Tasks, and Devices — reducing drop-off at entry.

Tasks

Binary one-time to-dos: submit PAN, add shop address, convert to daily settlement. Completable in under 5 minutes.

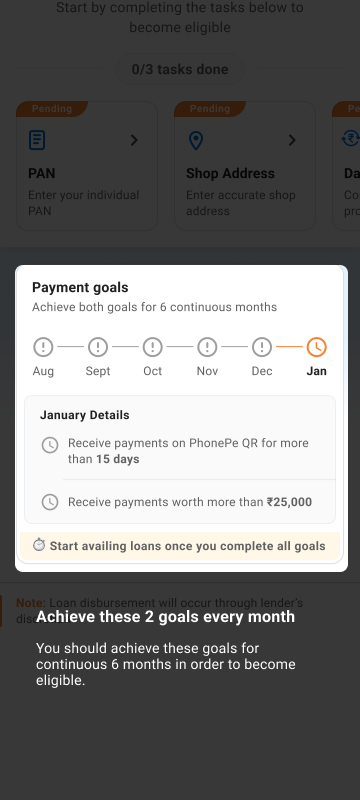

Milestones

Collect ₹25,000/month and stay active for 15 days — for 6 consecutive months. Milestone progress becomes the merchant's reason to return.

Devices

Maintain 0 dues on owned SmartSpeaker or EDC. Also an upsell surface for merchants who don't own a device yet.

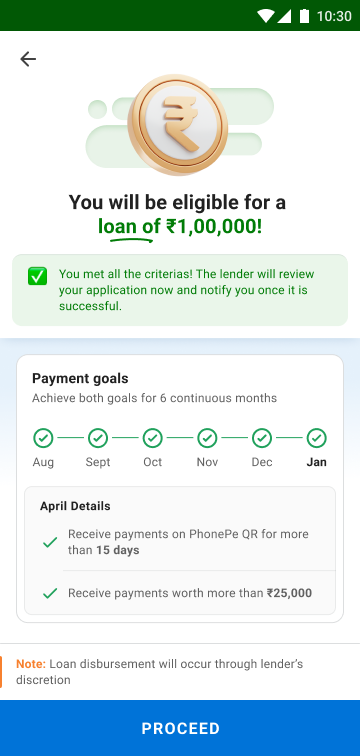

Application

Once all criteria are met, the merchant applies. 3rd-party lender reviews — approval rate of 60–80%, average loan of ₹1,00,000.

Manage

For established merchants who have availed devices and services, management is critical. The profile and settings architecture was rebuilt into two clear buckets — Business Settings and App Settings.

Account & QR

Show QR, Order QR, Update KYC, and Bank Account — the most-needed account actions — surfaced directly on the home screen.

Device management

Track orders, troubleshoot SmartSpeakers with a real-time diagnostic flow, pay device dues, and explore upgrades — all without calling support.

SmartSpeaker troubleshoot

A real-time device health diagnostic that fetches signal data from the device directly — replacing a flow entirely dependent on user-reported inputs.

Profile — 2 buckets

Business settings and App settings — clearly separated. T&C repositioned. Logout de-emphasised.

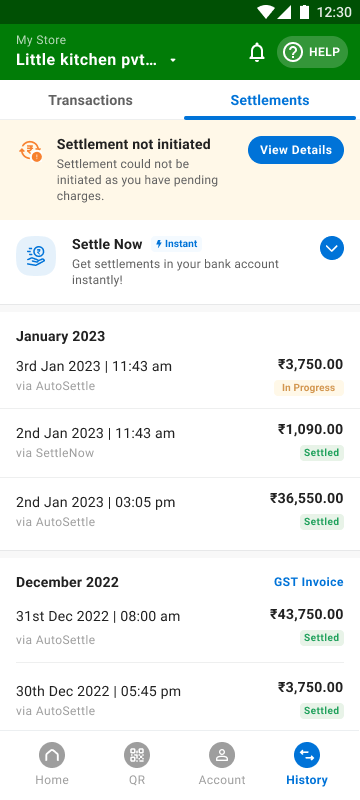

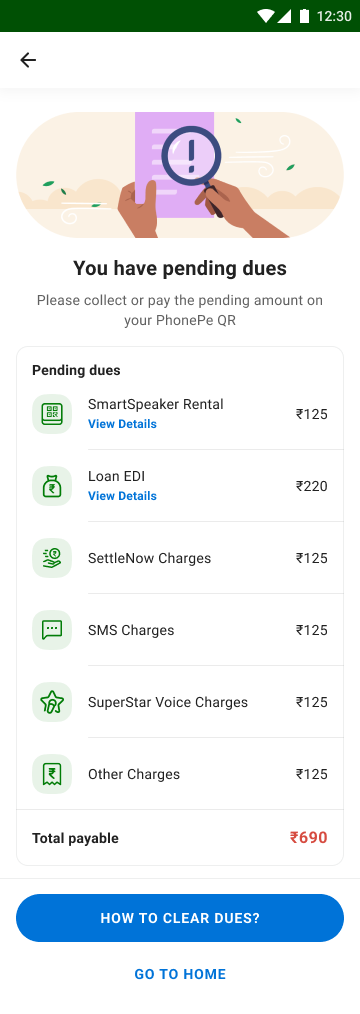

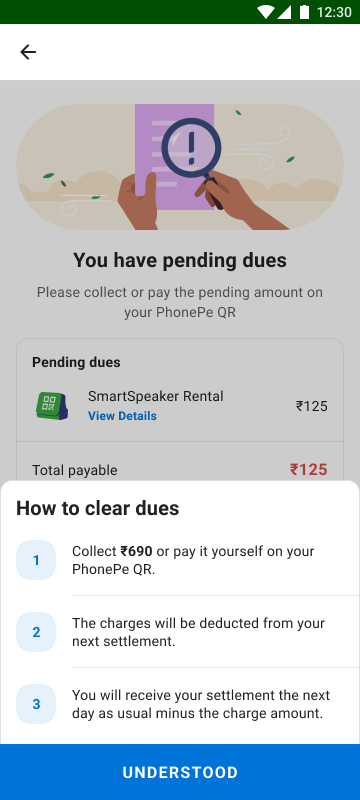

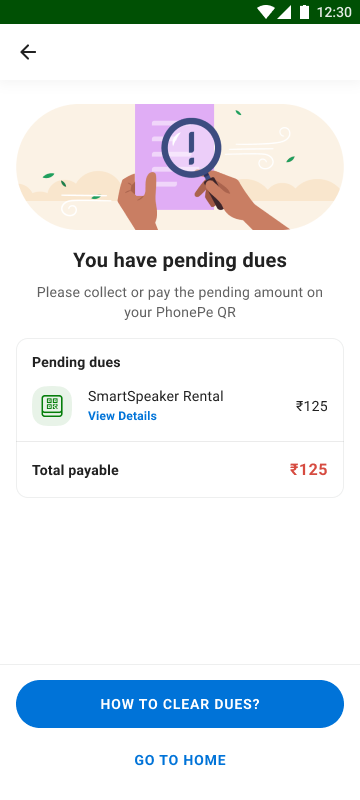

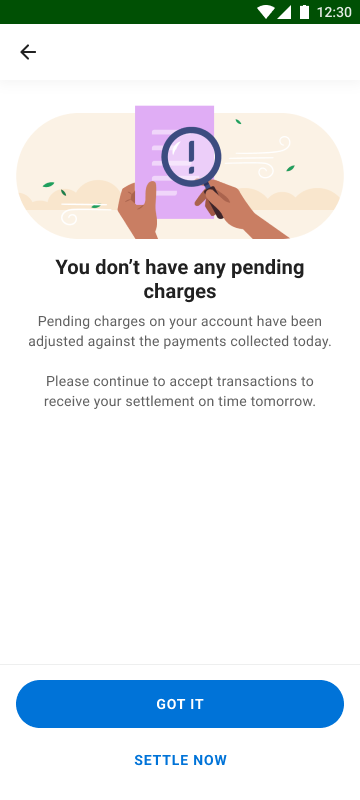

Settlement Not Initiated — a silent failure, made honest.

Merchants were seeing "this amount will be auto settled by 8 AM tomorrow" even when settlement couldn't happen due to pending charges. We corrected the messaging, added proactive home-screen ribbons with "View Charges" CTAs, and built a pending-dues explanation flow.

Settlements tab —

not initiated alert

Pending dues —

amount & CTA

Charge breakdown —

line by line

"How to clear" —

3-step explainer

Charges cleared —

settlement resumes

Lending top of funnel — a 6-month commitment merchants actually finish.

The eligibility journey outlined above needed two production flows: the top-of-funnel states a merchant moves through while working toward eligibility, and a guided first-time-use flow that explains the rules up front. Both are shown below.

Loan intro —

eligibility overview

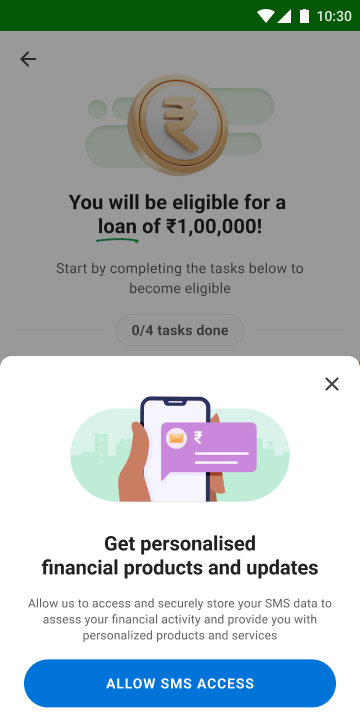

SMS permission —

personalised offers

0/4 tasks —

PAN & SMS pending

April missed —

goals in progress

All goals met —

apply now

First impression —

what loans offer

Task coachmark —

what to complete

Goals tooltip —

6-month commitment

SMS access —

personalised offers

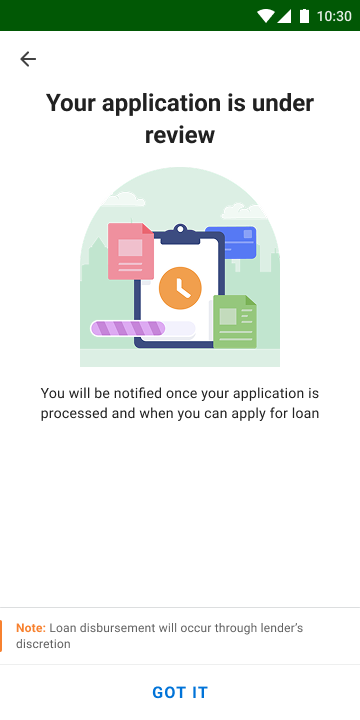

Under review —

lender notifies

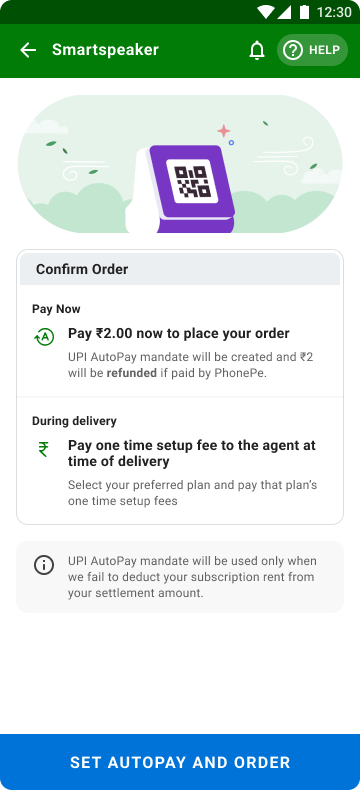

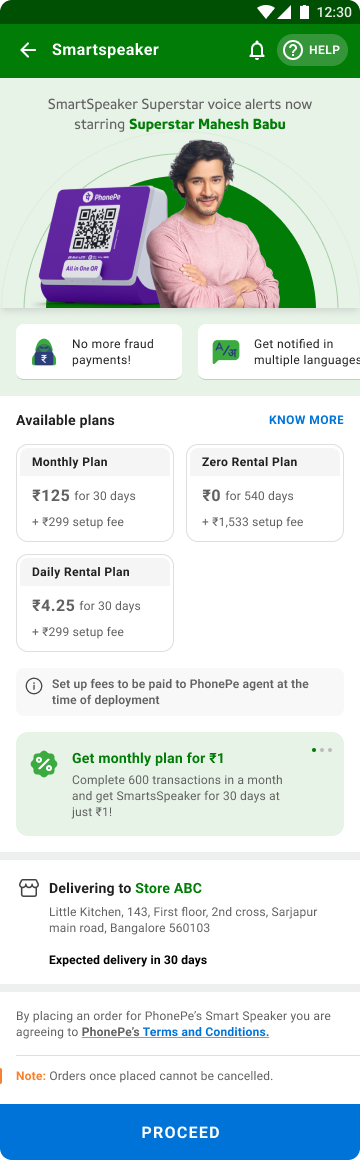

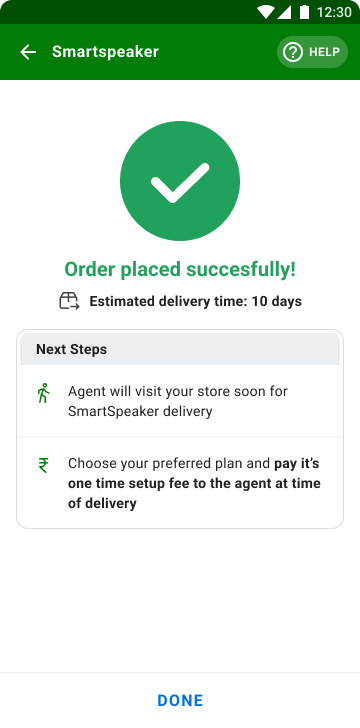

SmartSpeaker ordering — lowering the cost of saying yes.

The original device-purchase flow required full payment before dispatch — a friction point for cash-conscious merchants. We redesigned it around a ₹2 refundable AutoPay mandate to confirm intent, deferring plan selection and setup-fee payment to the point of physical delivery — reducing upfront commitment and improving order completion.

₹2 AutoPay mandate —

confirms the order

Plan selection —

superstar voice upsell

Order confirmed —

clear next steps

The rules we designed by.

Clarity over cleverness

Every element must earn its place. No decorative complexity, no ambiguous icons. If it doesn't serve the merchant's workflow, it doesn't belong on the home screen.

Always a way out

Keeping merchants trapped backfires. Clear escape hatches in every flow, no dark patterns, no forced funnels. Trust is built by giving control back.

Need to Want

Merchants come because they need the app. The design's job is to make them want to come back. Delight isn't decoration — it's return engagement.

Show, don't tell

Value-added services understood at a glance through illustrations. A merchant shouldn't need to read to know what a SmartSpeaker does for their business.

Right thing, right time

P0 on home is today's collection — not a loan banner. Context determines priority. The home screen adapts to what the merchant actually needs in that moment.

Transparency reduces anxiety

Merchants who don't know why their settlement didn't happen raise support tickets. Accurate, proactive messaging about settlement status is as important as the settlement itself.

Measurable impact across every metric that matters.

The redesign drove improvements across daily engagement, feature adoption, session time, revenue, and merchant satisfaction — validating the Conduct–Grow–Manage framework as a structural approach.

What I learned.

Design for the busiest moment

Merchants check this app between serving customers. The Conduct–Grow–Manage framework worked because it mirrors how they already think about their day — not how the org chart is structured.

Alignment is a design deliverable

With devices, loans, analytics, settlements, and QR all competing for home screen real estate, the framework became a shared language across product, engineering, and business.

Transparency reduces support costs

The biggest merchant anxiety wasn't a broken flow — it was silence. Merchants didn't know why their money wasn't in their account. Accurate, real-time messaging cost almost nothing to implement and had a significant impact on support ticket volume.

Revenue and UX aren't at odds

Surfacing value-added services in the right context improved both merchant experience and revenue. Merchants engaged because they saw value, not because they were trapped.

Gamification earns return visits

The Loan Eligibility journey introduced milestone-based progress that gave merchants a reason to open the app even on days they didn't collect a payment. Designing for consistent re-engagement within a 6-month window was as important as the final application screen.